How Compound Interest Works — And Why Starting at 25 vs 35 Is a $300,000 Difference

Compound interest isn't magic — it's math. Here's why a ten-year head start is worth hundreds of thousands of dollars.

Albert Einstein probably didn’t actually say that compound interest is the eighth wonder of the world. That quote gets pinned on him all over the internet, and there’s no real evidence he ever said it.

Doesn’t matter. The idea is still right.

Compound interest is the reason a person who invests $200 a month starting at 25 can retire wealthier than a person who invests $500 a month starting at 35, despite contributing far less total money. That outcome isn’t a motivational Instagram post. It’s straightforward math, and the numbers are worth knowing because they’ll change how you think about every dollar you invest.

What Compound Interest Actually Is

Simple interest means you earn a return on your original deposit. Compound interest means you earn a return on your original deposit and on all the interest you’ve already earned.

That second part is the magic. After year one of earning interest, your “principal” is larger than what you started with. In year two, you earn interest on that larger amount. In year three, you earn interest on an even larger amount. The gains are getting bigger even though the rate isn’t.

Over short periods, compounding barely matters. A dollar that grows 7% for one year becomes $1.07. A dollar that grows 7% for two years becomes $1.14. That’s almost exactly double the one-year return, so the compounding effect looks tiny.

But over long periods, compounding is everything. A dollar that grows 7% for 30 years becomes about $7.61. For 40 years, it becomes about $14.97. Going from 30 to 40 years nearly doubles the result, even though only 25% more time passed. That’s because the gains in the final decade are built on top of decades of previous gains.

The 25 vs. 35 Example, Worked Out

Let’s run the numbers. We’ll assume a 7% annual return, which is roughly the long-term average real return (after inflation) of the US stock market. We’ll ignore taxes and fees to keep the math clean.

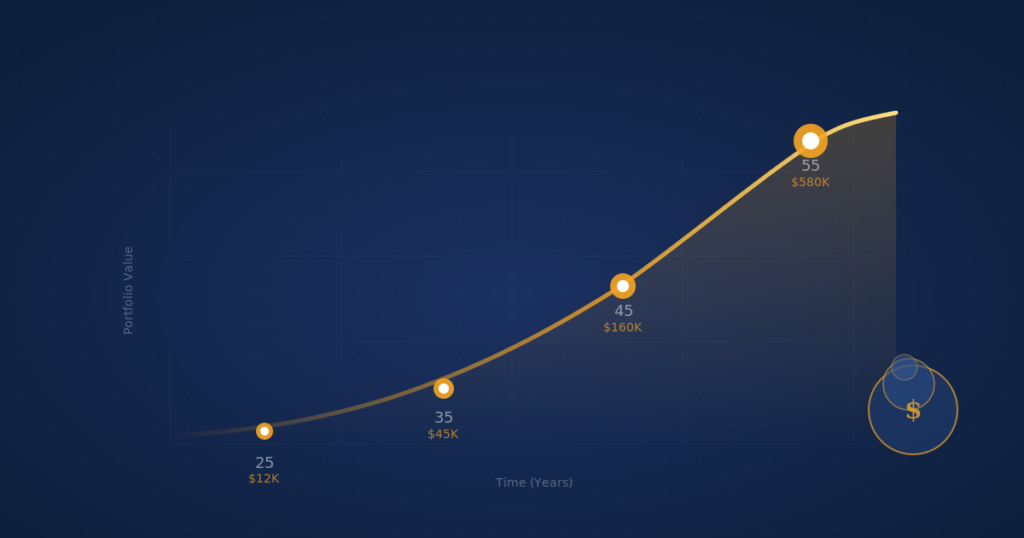

Person A starts at age 25. They invest $200 a month every month until they retire at 65. That’s 40 years of contributions. Total contributed: $96,000. Final value: roughly $525,000.

Person B starts at age 35 — ten years later. They invest $500 a month every month until retirement at 65. That’s 30 years of contributions. Total contributed: $180,000. Final value: roughly $612,000.

At first glance, Person B wins — they end up with more money. But look at the contributions. Person B invested $84,000 more than Person A and ended up with only about $87,000 more at retirement. Person A earned $429,000 in growth on $96,000 of contributions. Person B earned $432,000 in growth on $180,000 of contributions.

Now flip the question. What if Person A kept their $200 monthly contribution but Person B matched it, also $200 a month? Person A ends up with $525,000. Person B ends up with about $245,000. A ten-year head start on the exact same contribution produces more than double the final balance. That’s the $300,000 difference.

The title isn’t hype. The math is just that aggressive at long time horizons.

Try It With Your Own Numbers

See what your money actually does over time — adjust the sliders below.

Why It Works This Way

The reason early dollars matter so much is that every dollar in a compounding account has its own timeline. A dollar invested at age 25 compounds for 40 years. A dollar invested at age 35 compounds for 30 years. A dollar invested at age 55 compounds for 10 years.

The dollar invested at 25 isn’t just earning 10 more years of returns. It’s earning 10 more years of compounded returns, which means it goes through many more doublings than a dollar invested later. (At 7%, money roughly doubles every 10 years. So a dollar invested at 25 doubles four times before retirement, becoming $16. A dollar invested at 55 doubles once, becoming $2.)

The dollars you invest in your 20s work for you for your entire adult life. The dollars you invest in your 50s work for you for a fraction of that. That asymmetry is what compound interest really is.

Why Starting Is More Important Than Optimizing

A lot of financial content focuses on getting the details exactly right: picking the perfect fund, shaving 0.05% off your expense ratio, finding the optimal rebalancing schedule. These things are worth doing. But they’re second-order.

A person who invests $100 a month into a mediocre fund starting at 25 will almost certainly end up better off than a person who waits until 35 to find the perfect optimized portfolio. Time in the market beats timing the market, beats picking the market, beats almost everything.

This is why financial advisors, when honest, keep telling you the same boring thing: start now, keep contributing, don’t stop during downturns. Those aren’t suggestions. They’re the rules that matter most, and the compounding math is why.

What If You’re Already Behind

Let’s say you’re 40 and you haven’t started. Or 50. Or 60. Does this mean you’re out of luck?

No. It means you have to compensate by contributing more aggressively, working longer, or accepting a more modest retirement lifestyle. Compound interest can’t create time you don’t have. What it can still do is work hard for whatever years remain.

A 50-year-old who aggressively saves $2,000 a month for 15 years at 7% ends up with around $622,000. That’s not the $525,000 Person A got from $200 a month over 40 years, but it’s close. The catch is that it takes a much higher contribution rate. You’re substituting money for time, and the older you start, the more money you need.

The second-best time to start is today. The best time was decades ago. There’s no third-best time.

The One Mistake That Breaks Everything

Compounding only works if you let it run. The biggest destroyer of long-term wealth is pulling money out during downturns, or stopping contributions when you get scared, or trying to time the market by selling high and rebuying later.

Every time you interrupt the compounding, you reset the clock on the money you took out. And in a diversified portfolio, the gains happen in bursts, usually clustered in a few big-return days per decade. Miss those days by being on the sidelines, and the math collapses.

The recipe is simple, even if the discipline is hard: invest consistently, never pull the money out unless it’s retirement, and ignore the headlines. That’s it. That’s compounding.

Frequently Asked Questions About Compound Interest

What is the Rule of 72?

The Rule of 72 is a shortcut for estimating how long it takes your money to double. Divide 72 by your annual return rate. At 7%, money doubles roughly every 10.3 years (72 ÷ 7 = 10.3). At 10%, it doubles every 7.2 years. The Rule of 72 makes it easy to see why starting early matters so much — each additional decade you give your money is another full doubling.

How often does compound interest compound in index funds?

In a stock index fund, compounding doesn’t happen on a fixed schedule the way a savings account works. Instead, the fund’s value grows (or falls) continuously as the underlying stocks move. Dividends are typically paid quarterly and, if reinvested, immediately start compounding. For practical purposes, think of it as compounding daily — every day the market is open, your gains from previous days are already part of the balance earning new gains.

What accounts use compound interest?

High-yield savings accounts, money market accounts, and CDs compound interest — usually daily or monthly. Index funds, ETFs, and individual stocks don’t pay “interest” in the traditional sense, but they grow through price appreciation and reinvested dividends, which produces the same compounding effect. Retirement accounts like 401(k)s and Roth IRAs are simply tax-advantaged wrappers — the compounding comes from whatever investments you hold inside them.

Is compound interest always good?

No — compound interest works against you when you’re the borrower. Credit card debt at 20% APR compounds just as aggressively as your investments, except it’s growing a balance you owe, not one you own. A $5,000 balance left untouched for 10 years at 20% APR becomes roughly $31,000. This is why paying off high-interest debt is the single best guaranteed return available — you’re stopping a compounding process that’s working in the wrong direction.

What is the difference between APR and APY?

APR (Annual Percentage Rate) is the interest rate without accounting for compounding within the year. APY (Annual Percentage Yield) is the effective rate after compounding is included. A savings account with a 5% APR compounded monthly has an APY slightly above 5%, because each month’s interest earns interest for the rest of the year. When comparing savings accounts, use APY — it’s the number that reflects what you’ll actually earn.

Quick Links

If this made you want to stop doom-scrolling and actually start investing, good. Subscribe to the KatchingStacks newsletter — one short, useful email a week about money without the nonsense. When you’re ready to take action, our How to Start Investing With $100 guide walks through the first step.

Ready to put this into practice? See our Best Robo-Advisors 2026 comparison to find a platform that fits your strategy.