What Is an Index Fund? (And Why Warren Buffett Won’t Shut Up About Them)

Index funds are the quiet backbone of modern investing. Here's what they are, why they work, and how Warren Buffett thinks about them.

Warren Buffett has made the same recommendation to regular investors for about forty years: buy a low-cost index fund, contribute to it regularly, and don’t touch it. He’s not being lazy. He’s made this argument with money on the line, and he’s won.

In 2007, Buffett bet a million dollars that a low-cost S&P 500 index fund would outperform a basket of hand-picked hedge funds over ten years. The index fund won, and it wasn’t close.

So what is an index fund, exactly? Why does a guy whose job is picking stocks keep telling everyone not to pick stocks? And what does this have to do with your actual money?

The Plain-English Definition

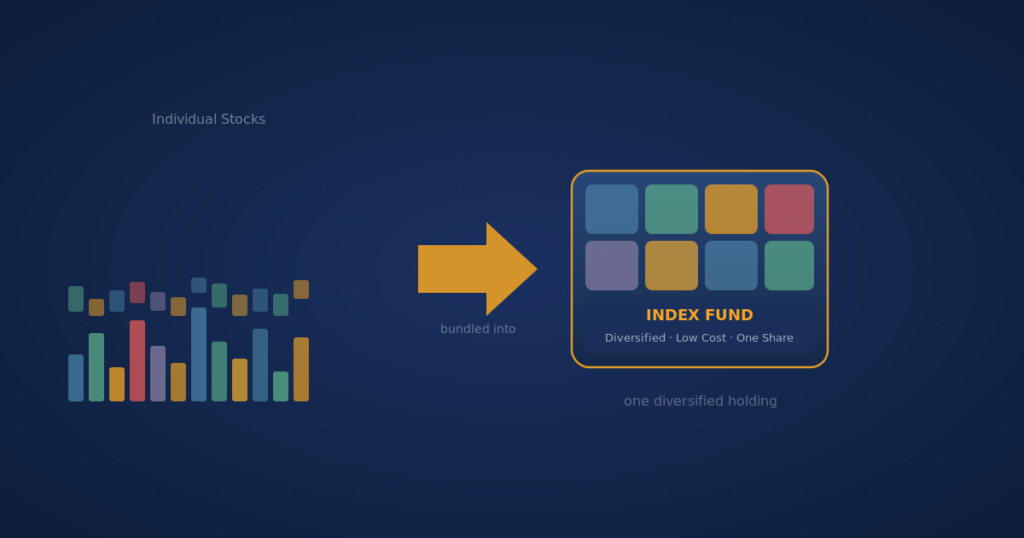

An index fund is a type of investment fund that tries to mirror the performance of a market index — a pre-existing list of companies — instead of trying to beat it.

The most famous index in the world is the S&P 500, a list of 500 of the largest publicly traded companies in the US. An S&P 500 index fund owns shares of every company in that index, in roughly the same proportions. If Apple is 7% of the S&P 500, then about 7% of the fund is invested in Apple.

The fund doesn’t try to figure out which of those 500 companies are going to do well next quarter. It just owns all of them. When new companies join the index, the fund buys them. When others drop out, the fund sells them. That’s it.

The alternative approach is an actively managed fund, where a portfolio manager picks individual stocks and tries to beat the index. These funds charge higher fees to pay for the research and the manager’s salary. The problem, which is now extremely well-documented, is that most of them don’t beat the index after you subtract those fees.

Why the Math Is So Brutal

Here’s the uncomfortable truth active managers don’t love to talk about. If you add up every dollar invested in US stocks, the average investor — by definition — gets the average return of the US stock market. That’s just arithmetic. For every investor beating the market, another is losing to it by the same amount.

Now subtract fees. Actively managed funds often charge around 1% a year. Index funds often charge 0.03% to 0.05%. Over decades, that difference becomes enormous because it compounds.

A $10,000 investment growing at 7% a year for 30 years becomes about $76,000 before fees. Subtract 1% in annual fees and you end up with about $57,000. Subtract 0.05% and you end up with about $75,000. The fee alone cost you $18,000 on a $10,000 starting investment.

This is why Buffett keeps repeating himself. The math is simple, the difference is huge, and most people still pay for active management because it feels smarter.

Types of Index Funds

Not all index funds are S&P 500 funds. There are index funds tracking all sorts of things.

Total stock market funds own the entire US stock market, which is thousands of companies rather than just 500. Total international funds own stocks outside the US. Bond index funds own the bond market. Sector index funds own specific slices, like technology or healthcare. There are even index funds that track specific themes or factors.

For most long-term investors, a small handful of broad index funds — a total US stock fund, a total international fund, and a bond fund — is enough to build a diversified portfolio. This is the famous “three-fund portfolio” that Bogleheads have been preaching about for decades.

ETFs vs. Mutual Funds

Index funds come in two main wrappers: mutual funds and ETFs (exchange-traded funds).

The differences are mostly structural. ETFs trade like stocks during market hours. Mutual funds trade once a day at the closing price. ETFs tend to be slightly more tax-efficient in taxable accounts. Mutual funds are sometimes better inside retirement accounts, where the tax differences don’t matter.

For the same underlying index, the performance is nearly identical. Don’t agonize over the choice. Pick a low-cost fund from a reputable provider, hold it, and move on.

How to Actually Own One

You can buy index funds through any brokerage — Vanguard, Fidelity, Schwab, or plenty of others. The three largest index fund providers are Vanguard, iShares (BlackRock), and Fidelity. Any of their broad-market funds is a defensible pick.

If you want it even simpler, robo-advisors like Betterment, Wealthfront, Fidelity Go, and Vanguard Digital Advisor build portfolios of index funds for you and rebalance automatically. You pay a small extra fee, but you don’t have to think about it.

What matters most isn’t which platform you pick. It’s that you actually start, keep contributing regularly, and don’t sell during downturns.

Why This Is Hard Despite Being Simple

The strategy fits in one sentence: buy a broad-market index fund, contribute regularly, hold for decades. The hard part isn’t understanding it. It’s sticking with it.

When the market drops 20%, every instinct screams at you to sell. When a hot sector like tech or crypto doubles in a year, every instinct says to abandon the boring index fund and chase the winners. The people who end up with real money 30 years from now are the ones who ignored both instincts and kept buying the boring fund every month no matter what the headlines said.

That’s the whole game. Most of what the financial industry sells you is a distraction from it.

The Buffett Summary

Warren Buffett’s instructions to the trustee managing his wife’s inheritance are famously simple: put 90% in a low-cost S&P 500 index fund and 10% in short-term government bonds. That’s it. No hedge funds, no stock picking, no market timing. From one of the greatest stock pickers who ever lived.

The lesson isn’t that picking stocks is impossible. It’s that most people who try to do it don’t beat the index, and the people who do beat it usually can’t repeat the feat. The index is a very difficult benchmark to beat, and an index fund lets anyone with a brokerage account own it for almost nothing.

That’s the argument. It’s been the same argument for decades because the math hasn’t changed.

Quick Links

Want more plain-English explainers on how money actually works? Subscribe to the KatchingStacks newsletter — one clear, jargon-free email a week. If you’re ready to put this into practice, our How to Start Investing With $100 guide walks through the exact steps.